My Dad's 'Die with Zero' Life

A few months before my dad’s passing in November 2024 I read Die with Zero by Bill Perkins, a book whose premise is that people should use their money to create “memory dividends” and enjoy life while they’re still physically and mentally able to, rather than being solely focused on saving for a future (e.g. retirement) with unknown twists and turns. In addition to saving all of my dad’s voicemails that he left me since 2017, I have also been mentally cataloguing his lifetime of various adventures and exploits, as I prepared myself for his decline and eventual passing. Though I don’t agree with all of the points made in Die with Zero, I have come to realize that my dad lived his life according to many of the tenets of the book that I now strive to live by. It seems that he instinctively understood what many struggle to learn: that life’s richest rewards come from experiences pursued at the perfect moment, not from what we cautiously save and look forward to “someday.”

Early Life

Born and raised in Greenwich, Connecticut, my dad adored his mom, tolerated his older sister, and had a rocky relationship with his dad. He loved sailing, his Porsche speedster, and motorcycles. After graduating from University of Pennsylvania’s Wharton School of Business he started his adventures by serving his country as a Marine in Vietnam. After two years of service, and a padded bank account from countless evenings of poker earnings, he took advantage of a benefit offered by the Marine Corps covering airfare for 1 year of circuitous, round the world travel, ending upon touching foot back in CONUS (continental United States). Instead of following the expected path of settling into a conventional career, my dad chose to embark on a round-the-world adventure. Except, he didn’t make it back to CONUS as soon as expected. After multiple stops in Asia and Australia, he stopped and ultimately settled in Europe, first in Garmisch, Germany, and later in St. Anton, Austria. There, he found new passions for downhill skiing, the German language and Bavarian mountain culture.

Instead of following the expected path of settling into a conventional career, my dad chose to embark on a round-the-world adventure.

My Dad’s passion for skiing started in the Bavarian Alps of Germany.

Perfect Timing for Love

A couple years into his European mountain life, Dad was hanging out at the Alber boot shop in St. Anton when he met a striking American woman visiting from Washington State. They quickly fell in love and were married stateside six months later in Bellevue, Washington. Clearly Dad had great instincts and knew not to delay when something truly mattered. After their wedding vows my parents began their life adventures together by moving to San Francisco’s Haight-Ashbury district in the height of the swinging 60s.

Building Memory Dividends: The Alpental Investment

After a few years of living the hippy life in San Francisco they moved back up to Washington to be closer to my mom’s family, then brought me and two afghan hounds into the picture soon after. Perhaps the best example of my dad’s (and mom’s) investment in “memory dividends” was the purchase of our Alpental Valley ski condo at Snoqualmie Pass in 1979 when I was 5 years old. This wasn’t just a real estate investment—this was an investment in a lifetime of mountain experiences together as a family doing what we love most – skiing! Every winter weekend was spent at Alpental, filled with skiing during the day and social gatherings in the evenings. Some of my most vivid childhood memories include waking up early to the shaking of the entire building as the ski patrol dropped avalanche bombs while I watched my Saturday morning cartoons. I clearly remember my parents’ excitement for the powder runs to be had that day.

This wasn’t just a real estate investment—this was an investment in a lifetime of mountain experiences together as a family doing what we love most – skiing!

The Alpental condo became more than a weekend getaway; it was the cornerstone of our family’s lifestyle and the hub of an extended family of fellow ski enthusiasts. Dad’s choice to make this investment when he did—when he was physically active, when I was young, and when we had years ahead to enjoy it—shows his understanding of seizing an opportunity when you can in order to build lasting memories.

A Life of Service

After his two-year stint in Vietnam, my dad continued his commitment to service by joining the Alpental Volunteer Ski Patrol in 1976. Known for the smell of his pipe (and later cigars), you could smell him from a mile away as the smoke wafted through the air on his ride up the chairlifts. A role that he served in for 20 years, this helped to further weave our family into the fabric of the Alpental community we loved. He also volunteered with Little Bit Therapeutic Riding Center, an organization that aims to improve the lives of children with disabilities through activities with horses.

Evolving with Life’s Seasons

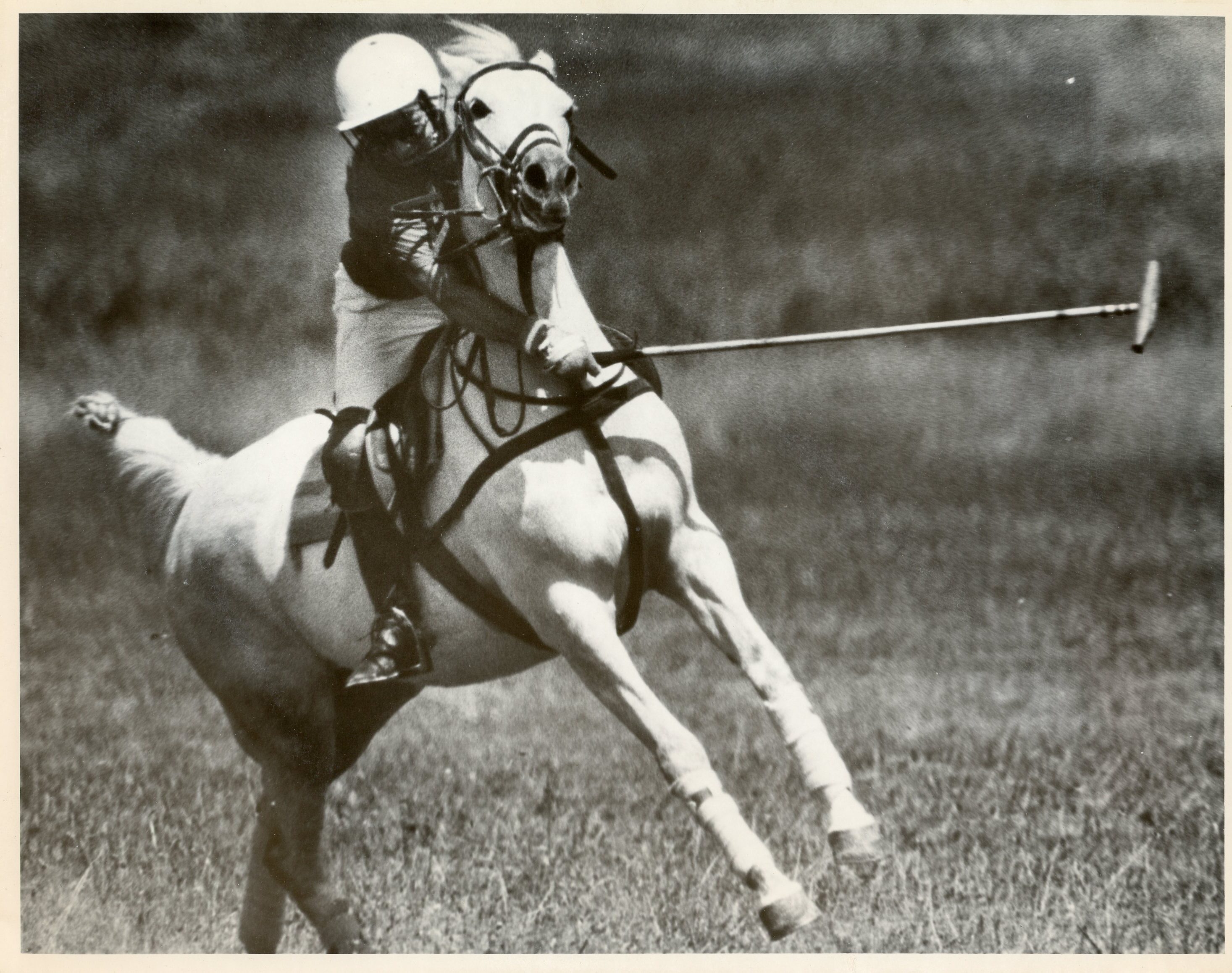

While skiing was his winter pastime, the sport of polo became his spring and summer pastime in his late 30s and 40s while still physically able. Then, recognizing shifting capabilities and desires, he shifted from polo to golf at 50, a sport that gave him joy for nearly three decades. He demonstrated how different activities suit different life stages, and the importance of timing them right.

He demonstrated how different activities suit different life stages, and the importance of timing them right.

Making the Most of Every Stage

Even when a stroke at 72 changed what he could do physically, he had already built a rich repository of experiences that provided him with years of story-telling. He’d wisely invested in activities when his body could fully participate, leaving him with a wealth of memories rather than regrets about missed opportunities.

Life on the (Financial) Edge

At the end of the book even the Die with Zero author admits that it is not prudent to aim for zero funds by your last day of life. It is about finding the right balance of when to spend your money based on when it will add the most value to your life. Some in the financial advice profession (including myself) might say that my Dad lived a little too close to the edge of his means, spending too much and not saving enough. He did manage to maintain a modest cushion of retirement funds to the end, which I’m sure he would argue was skill, but I would argue was also a fair amount of luck. He was very fortunate in successfully avoiding the expensive costs of long term care. Thanks to my mom as his doting caregiver who assisted him with activities of daily living, he was able to gracefully age-in-place during his final years on beautiful Pine Lake.

This motivates me to continue connecting with my wise, 90-year old self to ask the question: How can I be using my money right now to build those adventure-filled memory dividends with friends and family, and live a life with no regrets?

The Legacy He Left Me

This process of reflecting on my dad’s life and its parallels with the Die with Zero principles has elevated my respect for him, as our relationship was not always as rosy as the descriptions above may sound. His pursuits often pulled him away from me and my pursuits, as he would go one way with his horse trailer to polo tournaments and my mom and I would go the other way with ours to my horse shows, sometimes leaving me feeling unsupported. He at times would criticize my life choices, for example when I chose to move to the French Alps in my mid-20s to become a ski bum, leaving my college education and a good corporate job behind (sound familiar?). Thankfully he had passed on his strong-willed and adventurous spirit, as I stuck to my guns and didn’t listen to him while making those life-changing decisions. In his later years, as his ego declined and his sentimentality increased, he commended me for those decisions. So much of who I am was inherited from him – the love of adventure and travel, the curiosity to meet new people and cultures, the determination to learn a 2nd language, desire to maximize physical capabilities, the love for animals – and for that I am eternally grateful. He never voiced any regrets about his life. This motivates me to continue connecting with my wise, 90-year old self to ask the question: How can I be using my money right now to build those adventure-filled memory dividends with friends and family, and live a life with no regrets?

In Loving Memory of A.C. Walker – “Dad”

May 28, 1940 – November 25, 2024

The Long Game: Lessons from Aging Athletes for Long-Term Investors

As I watch veteran athletes in mountain sports continue to push their limits well into their 40s, 50s, and beyond, I can’t help but be inspired. Some of these mountain warriors are engaged in competition, such as ski mountaineering races, pushing their limits to see what their bodies can do. Others are mountain guides who are not only keeping their clients safe, but also helping these clients achieve their life goals. Others are out there pushing themselves physically purely to continue doing what they love, while also spending time with friends and family. The requirements to continue an active, mountain lifestyle until late in life offer valuable insights that extend far beyond the trails and slopes – particularly when it comes to long-term investing. Below we explore some key parallels between the journey of a veteran mountain athlete and the path of a savvy long-term investor.

By starting early, young investors can set their future selves up for increased flexibility, which could take the form of a mid-career sabbatical, college savings for children, or funding an earlier retirement.

Start Early to Build a Strong Foundation

Though it’s never too late to start, building a strong athletic foundation in your 20s and 30s creates a physiological ‘savings account’ for mountain sports enthusiasts. During these prime years, your body is optimal for developing muscle mass, cardiovascular endurance, and neuromuscular connections. This early investment in fitness helps maintain higher baseline strength and endurance as you age, potentially delaying the onset of age-related performance decline. The habits and discipline formed during this period often translate into lifelong commitments to health, allowing athletes to continue pursuing their mountain passions well into the later years of life.

Starting to invest early in your 20s and 30s – even with small amounts – can have a profound impact by harnessing the power of compounding. Just as young athletes build strength and technique over time, early investors can build a robust portfolio that can weather market fluctuations more easily with the benefit of time on their side. By starting young, investors have the opportunity to set their future selves up for increased flexibility, which could come in the form of taking a mid-career sabbatical, college savings for children, or funding an earlier retirement. In both realms, the message is clear: the earlier you start building your foundation, the greater your potential for long-term success in reaching your financial goals.

The Importance of Consistency and Discipline

Many successful aging athletes credit their longevity to dedicated discipline and consistency in training, nutrition, and recovery. They understand that maintaining optimal performance requires near daily commitment, even when motivation wanes or results aren’t immediately visible. Being consistent includes modifying one’s pursuits in later years with an eye to sustainability and avoiding injury. Depending on age, a fall resulting in injury could lead to physical decline.

Long-term investors face a similar challenge. Starting with a well-thought-out, passive investment strategy that avoids trying to beat market returns – and sticking to it even during market downturns – often yields the best results over time. Successful long-term investors are able to cut out the noise of get-rich-quick schemes found on social media, financial news networks, and maybe a well-intentioned brother-in-law who is trying to sell them on the next fancy financial product. Like a trail runner’s consistent training through all seasons, regular, disciplined investing can compound into significant gains over the years.

Successful long-term investors are able to cut out the noise of get-rich-quick schemes found on social media, financial news networks, and maybe a well-intentioned brother-in-law who is trying to sell them on the next fancy financial product.

Don’t forget Recovery and Patience

Rest and recovery become increasingly crucial for aging athletes. They need more time between intense efforts to perform at their best and avoid injury, especially for those involved in higher-impact sports. This patience and self-care can contribute significantly to one’s athletic sustainability.

For investors, the concept of recovery and patience translates to maintaining a long-term perspective and resisting the urge to constantly tinker with investments as the stock market waxes and wanes. Allowing investments time to grow, resisting the temptation to react to every market fluctuation, and patiently waiting for strategies to bear fruit are key to long-term success.

Building a Team

Behind every successful aging athlete is a supportive team, such as a coach, physical therapist, doctor, and friends and family. This support system helps the athlete maximize their potential and navigate the challenges of a long athletic career.

Long-term investors can benefit from building their own (financial) team. This might include a financial planner, tax professional, estate planning attorney, and even like-minded peers who share their experiences. A strong support system can provide valuable perspectives, help avoid costly mistakes and offer encouragement and guidance during tough market conditions.

By staying true to their personal “race,” investors can maintain a steady course through market volatility, make more rational decisions, and build wealth in a way that aligns with their specific needs and lifestyle.

Run Your Own Race

As an aging athlete it becomes increasingly important to focus on personal goals rather than comparing oneself to younger competitors or past achievements. By adapting their training and leveraging their evolving strengths (such as improved endurance and tactical wisdom) this will aid in success and fulfillment by celebrating personal victories, regardless of whether they land a podium spot.

Long-term investors can stay on track with their financial goals by adhering to their own tailored financial plan that is aligned with their individual goals and values, rather than chasing market trends or comparing themselves to others. This includes crafting an investment plan constructed for their unique goals, risk tolerance, and time horizons. By staying true to their personal “race,” investors can maintain a steady course through market volatility, make more rational decisions, and build wealth in a way that aligns with their specific needs and lifestyle. In both realms, running your own race leads to a more sustainable, enjoyable, and ultimately successful journey.

Enjoy the Journey

Finally, adapting one’s training to a program that is truly enjoyable can aid in ensuring a successful, long-term athletic career. Incorporating friends and family in activities adds a social aspect that will help get you out the door for those early morning objectives. Many aging athletes speak about rediscovering their love for their sport as they near the end of their competitive careers. Free from the pressure of constantly proving themselves, they find renewed enjoyment in the simple act of moving through the mountains.

With investing, it can be challenging to strike the right balance between prudently saving and investing for the future, but also enjoying your hard-earned dollars now. A helpful exercise to find this balance is to focus on your eulogy virtues rather than resumé virtues. Imagine yourself at age 90, relaxing in a rocking chair on the porch of your mountain cabin, reflecting on your life and accomplishments. What actions, experiences, purchases and connections that you make NOW will positively build the memory dividends that will carry you into later life?

What actions, experiences, purchases and connections that you make NOW will positively build the memory dividends that will carry you into later life?

Conclusion

The parallels between veteran mountain athletes and long-term investors are striking. Both pursuits require discipline, patience, consistency and commitment. By adopting the mindset of a seasoned mountain athlete – leveraging a strong foundation, staying true to personal goals, and focusing on the long game – investors can navigate the complexities of the financial world with greater confidence and success.

Remember, just as a mountain athlete’s career is measured not by a single race or accomplishment but by their entire body of work in challenging environments, successful long-term investing is about consistent performance over years and decades. By applying these lessons from the world of mountain sports, investors can build a robust, adaptable strategy that stands the test of time and helps achieve their long-term financial goals.